TD SYNNEX: The Distributor With a Hidden AI Infrastructure Business

TD SYNNEX trades at a blended distributor multiple. Inside it sits a hyperscale ODM with programs across all five top US hyperscalers, growing operating income at 66% YoY.

TD SYNNEX is one of the world’s largest IT distributors, they connect over 2,500 technology vendors to 150,000 resellers, integrators, and managed service providers across 100+ countries. When a business buys Cisco networking gear or Microsoft software through a reseller, there’s a good chance TD SYNNEX is somewhere in that transaction. At $60+ billion in annual gross billings, it’s an enormously valuable network and the vendor relationships and customer infrastructure built over four decades are not easy to replicate.

That distribution core is now evolving in two directions at once. The first is a mix shift within distribution itself, away from commodity hardware and toward higher-margin software, security, and cloud solutions with recurring revenue characteristics. The second is Hyve Solutions: a custom hyperscale ODM that designs, manufactures, and deploys purpose-built AI infrastructure for the world’s largest data center operators. Different business model, different customers, different growth rate 95% gross billings growth last quarter, with programs now secured across all five of the top US hyperscalers.

These structural shifts are not yet reflected in how the market values the business. Margins are expanding, the earnings beat cycle is accelerating, and the analysts are only beginning to revise their models upward. The stock still trades at roughly 12.5x (around 10 before Q1 numbers) forward earnings, a multiple that makes sense for a mature distributor, but not for a company whose AI infrastructure arm just doubled its supply chain services revenue YoY. The opportunity is in the re-rating.

The Revenue Mix Shift

For most of SNX’s history, the revenue mix reflected the IT industry’s center of gravity. They sold personal computers, printers, peripherals, and commodity servers. High volume, low complexity products with low margins and predictable refresh cycles. The distribution economics were easy to understand.

That mix is now shifting structurally. In Q1 FY2026, Advanced Solutions, which covers data center infrastructure, hybrid cloud, security, networking, and software grew 19% YoY to $12.4 billion in gross billings, outpacing Endpoint Solutions and now representing the majority of distribution revenue. The margin economics across these two categories are fundamentally different. Security software carries recurring revenue characteristics. Enterprise AI infrastructure projects span GPU servers, high-speed networking, cloud connectivity, and managed services, and configuring that stack requires solution-level expertise that commands better economics than a commodity hardware transaction.

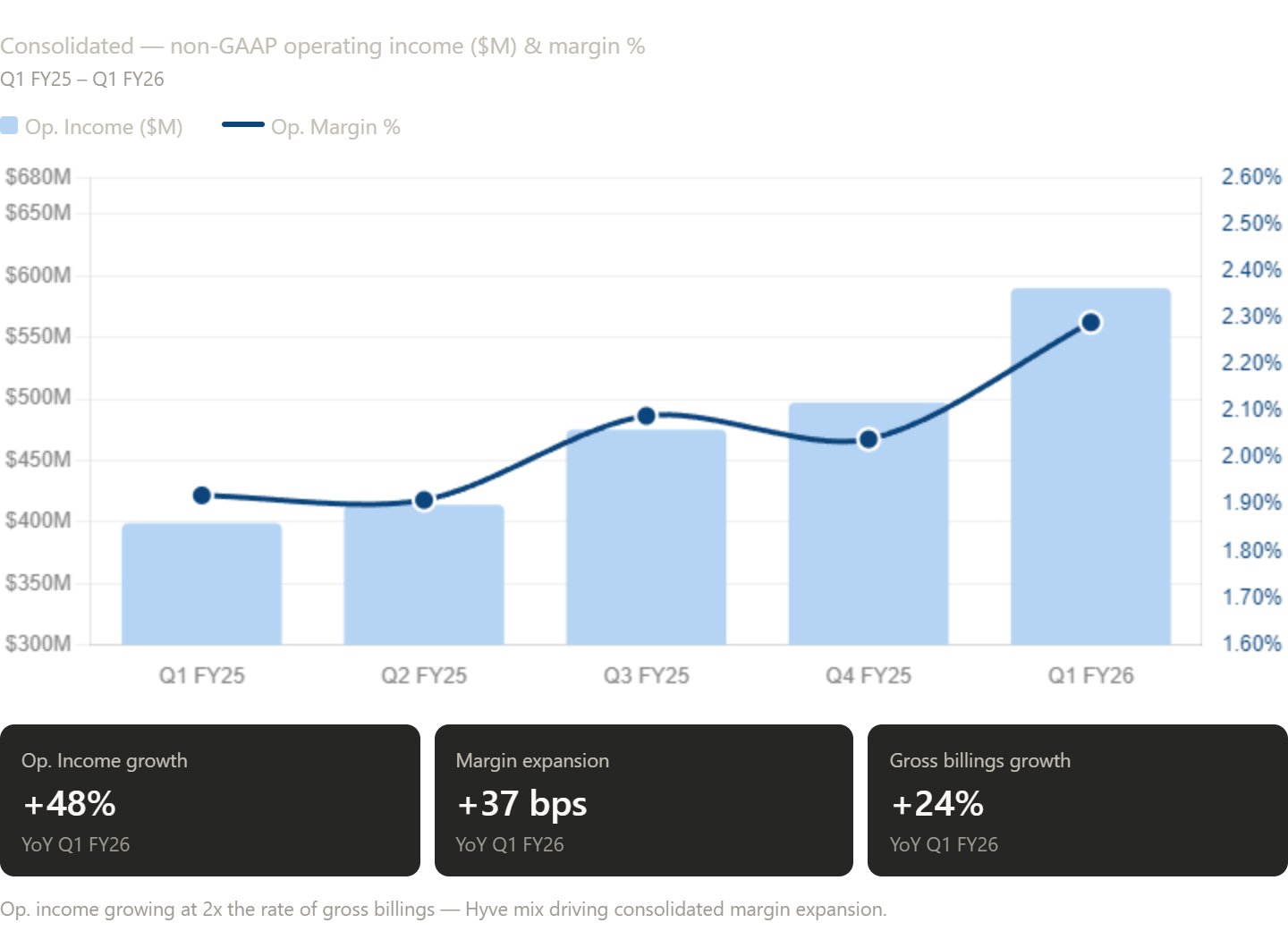

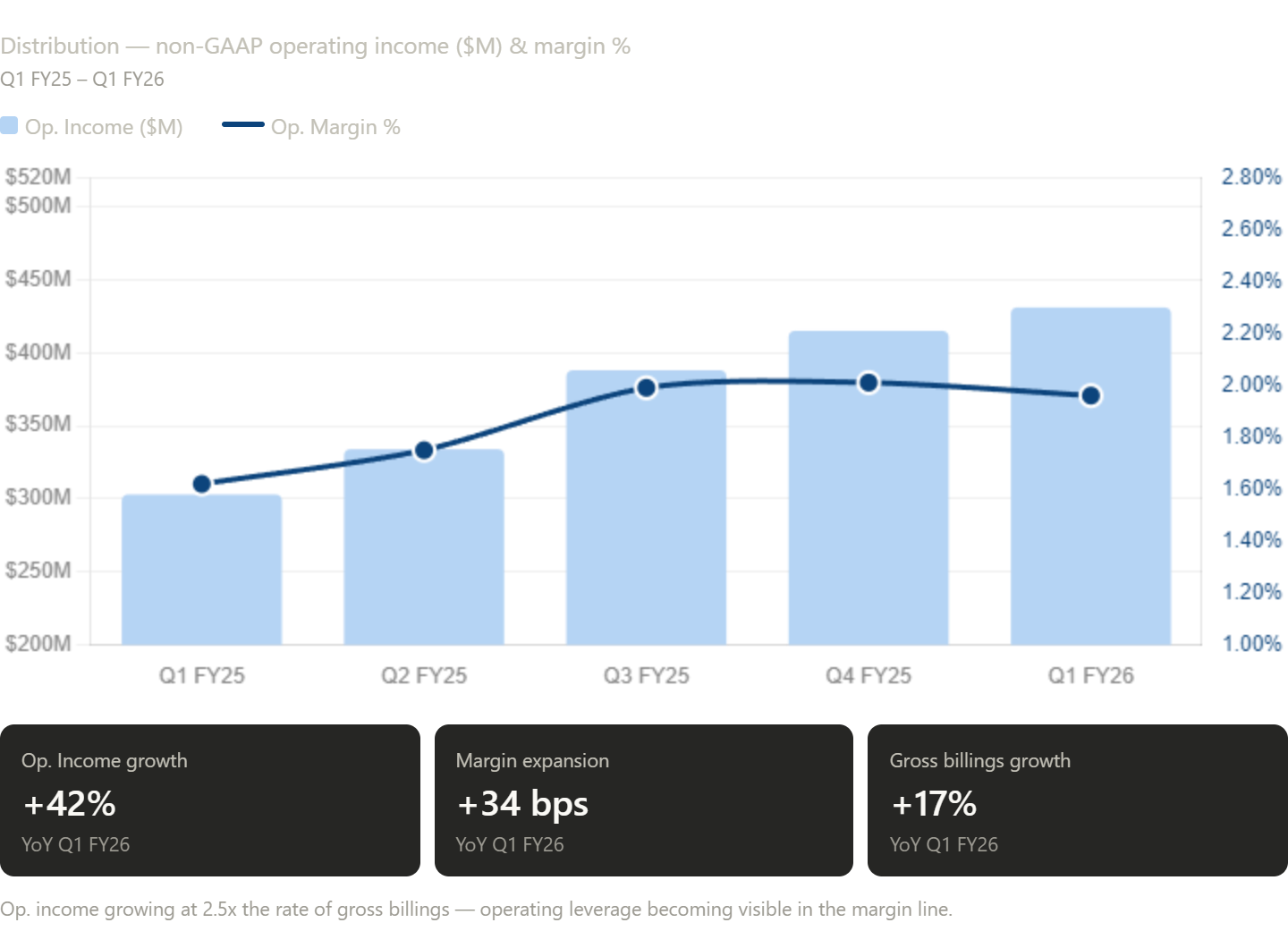

The financial consequence is showing up in the numbers. Distribution operating income grew 42% YoY in Q1 against 17% gross billings growth. Operating leverage is becoming visible as higher-margin categories take a larger share of the revenue base. The mix shift has a long runway, and the margin structure is only beginning to reflect it.

The Hidden Gem

Hyve is an original design manufacturer. They partner directly with hyperscale cloud operators to engineer, manufacture, and deploy custom compute infrastructure purpose-built for their specific workloads. These are rack-level systems designed from the ground up to meet a hyperscaler's exact thermal, power, networking, and performance requirements, then manufactured at scale and integrated into their data center infrastructure.

When a hyperscaler decides to build a new generation of AI training or inference infrastructure, they don’t simply place a purchase order. They begin an engineering program, a multi-month, sometimes multi-year collaboration with a small number of trusted ODM partners to define specifications, qualify components, test thermal and power characteristics, iterate on design, and ultimately certify a platform for mass deployment. The ODM partner is embedded in that process from the earliest stages.

This is what makes Hyve’s position structurally different from commodity distribution. By the time product ships, Hyve has co-developed the design with the customer. Their engineers have been inside the customer’s infrastructure roadmap. They understand not just what is being built today but what comes next. The relationship is not transactional, it is a continuous engineering partnership that deepens with every program cycle.

The switching costs embedded in this model are substantial. Replacing an ODM mid-program means re-qualifying components, re-certifying thermal and power characteristics, retraining integration teams, and absorbing the schedule risk of a transition during an active infrastructure buildout. For a hyperscaler spending tens of billions on data center capacity annually, that risk is not worth taking for marginal cost savings. Programs, once established, tend to persist and expand.

Future of Hyve

Management has been explicit about the strategic direction of Hyve. They’re moving up the value chain toward more complete system-level solutions by integrating traditional compute, accelerated compute, networking, and storage into unified rack-scale platforms. The progression from component assembly toward full system integration means higher engineering content per program, deeper customer integration, and better margin economics over time.

The addressable market expanding into accelerated compute is the key variable. AI training clusters require not just custom servers but custom networking fabrics, power distribution systems, and cooling infrastructure, all of which need to be co-designed and co-validated. As hyperscalers push toward larger and more complex AI clusters, the scope of what an ODM partner needs to deliver expands. Hyve’s targeted investments in engineering and manufacturing capability are positioning it to capture that expanding scope rather than being displaced by it.

A growing pipeline of new program opportunities, validated by the two new hyperscaler wins in 2026. With programs now across all five top US hyperscalers and active investment in engineering capability, Hyve is building the foundation for a multi-year revenue ramp that the current financials are only beginning to reflect.

Sum-of-the-parts Valuation:

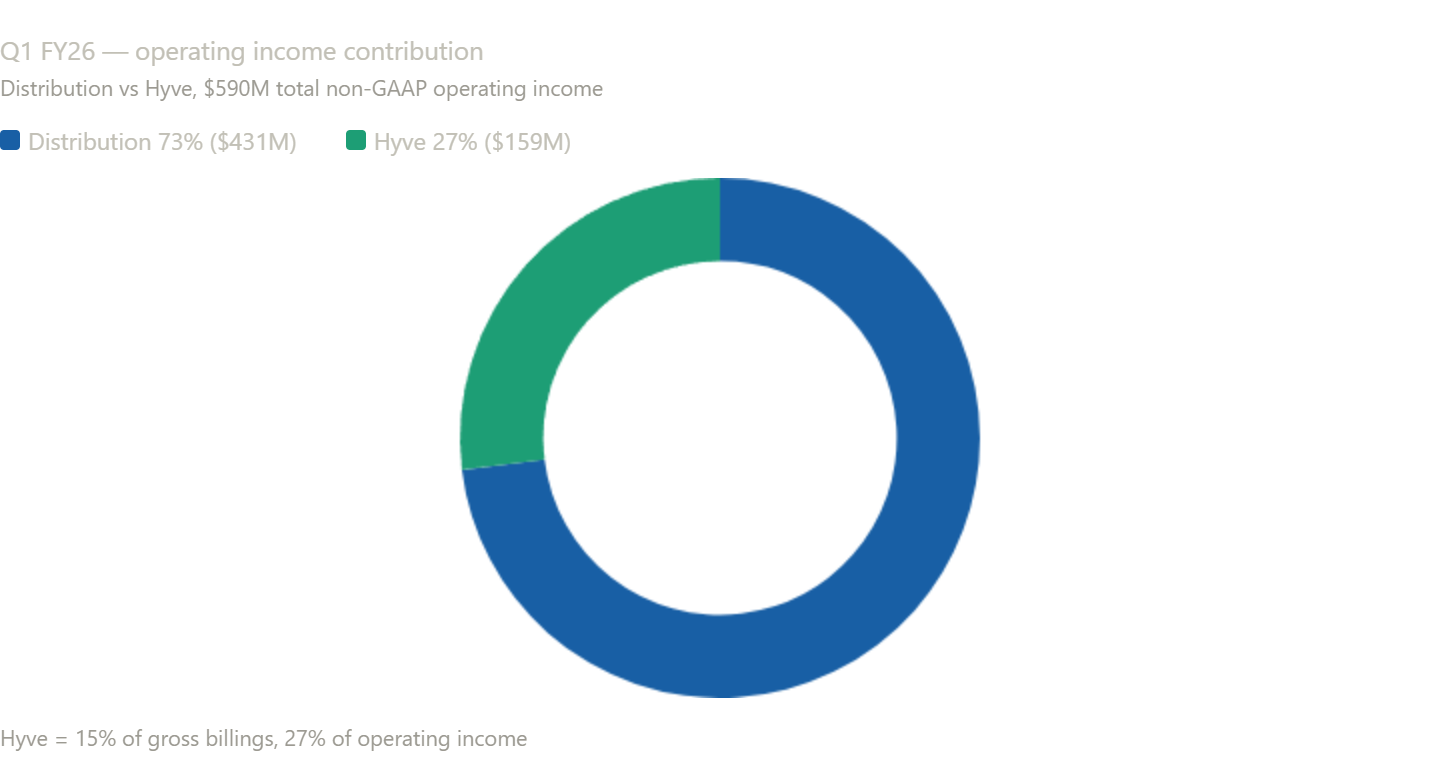

Starting this quarter, Hyve reports as a standalone segment for the first time. Previously consolidated within the Americas distribution segment, its revenue, margins, and operating income were invisible to anyone not digging through management commentary. That lack of visibility is a large part of why the market has not priced it correctly. Now that the numbers are in plain sight, the gap between what Hyve is worth and what the market is ascribing to it becomes very difficult to ignore.

Distribution segement:

Distribution is a high quality IT distribution business growing operating income at 42% YoY with expanding margins, Microsoft Frontier designation, and deepening mix toward software, security, and cloud. This is aswell as Hyve a growing part of the revenue and EPS, but is more mature.

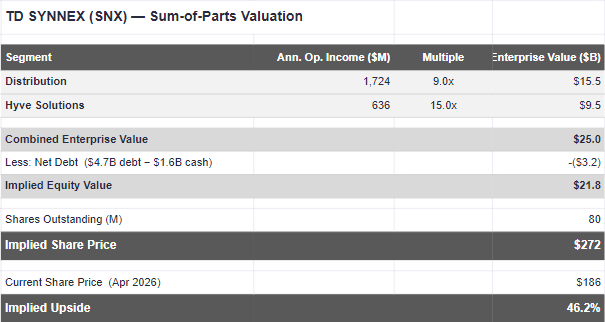

The closest public comparable is Ingram Micro, which has historically traded at 8-10x operating income. Arrow Electronics trades at a similar range. By applying 9x to SNX’s distribution run rate (a slight premium to the peer midpoint reflecting the vendor relationship quality and the mix shift underway) it gives the distribution segment an enterprise value of approximately $15.5 billion ($1.72Bx 9).

That figure alone is roughly equivalent to TD SYNNEX’s entire current market capitalization. Which means at today’s price, you are acquiring Hyve for approximately zero.

Hyve segment:

Hyve is a hyperscale ODM generating $636 million in annualized operating income, growing at 66% YoY, with programs across all five top US hyperscalers and two newly signed customers not yet at full volume. This is the highest-growth part of the business and the one the market has consistently underpriced by collapsing it into a blended distribution multiple. As Hyve grows and takes a larger part of the total revenue, we will see a further expansion in the blended margins as well as a higher multiple.

Using enterprise value divided by operating income, and the peer range for businesses with Hyve's profile is 12-20x. Celestica, the most direct public comparable, trades at the top end of that range. If we use 15 operating income multiple (somewhere in the low end) the math is simple. If we use $636 million in annualized operating income multiplied by 15 equals approximately $9.5 billion in standalone enterprise value. That multiple applies no premium for the two new hyperscaler programs not yet at full volume and assumes no further operating income growth. It is a deliberately conservative entry point, and it implies that the market is currently ascribing close to zero value to a business that by any standalone measure would be a very interesting play on the AI infrastructure buildout.

Valuation

By combining the sum-of-the-parts EV of the two segments and netting out $3.2 billion in net debt, we get an implied equity value of $21.9 billion and an implied share price of $272, representing approximately 46% upside to where the stock trades today. That figure is built on multiples that sit at or below where the direct peers trade, using current run-rate earnings with no forward growth assumption on either segment.

The sum-of-parts is not the only lens that shows the mispricing. On a straight earnings basis, SNX trades at approximately 12.5x FY2026 consensus EPS of $14.86 a multiple more consistent with a business in secular decline than one that just delivered 69% EPS growth YoY and guided 34% EPS growth for Q2. The share count is also actively shrinking, SNX repurchased approximately $80 million of stock in Q1 alone, mechanically compounding EPS growth independent of underlying earnings expansion. A growing business, expanding margins, a declining share count, and a 12.5x forward multiple.

The gap between $272 and $186 exists because the market has never had to price these two businesses separately. Four quarters of standalone Hyve data will make the blended distributor multiple increasingly difficult to justify and the implied upside increasingly difficult to ignore.